Key takeaways

- The Wayfair ruling replaced Quill’s physical presence rule: Businesses must now collect and remit sales tax in states where they exceed $100,000 in sales or 200 transactions, even without a physical presence.

- States gained broader taxing authority: The decision opened the door for all states to enforce economic nexus laws, increasing compliance obligations for online sellers.

- Small businesses face new compliance challenges: While large retailers are mostly prepared, smaller e-commerce businesses may need accounting support and automation tools like LumaTax to stay compliant.

Going into the Supreme Court’s hearing of the South Dakota v. Wayfair case, which was argued back in April, one thing was certain: something had to give. In the increasingly complicated legal environment of states struggling to expand their sales-tax reach while bumping up against an old ruling, more clarity was needed for some time.

At a time when compliance with use-tax laws is low, and online retail sales last year grew to over $453 billion, states believe they’re missing out on billions of dollars in uncollected tax money.

Now the decision has been made to overturn the 1992 Quill Corp. v. North Dakota ruling, allowing South Dakota to throw out the physical-presence determination and institute a threshold rule for online businesses who make sales to residents of their state. This means online sellers have legal nexus and must collect sales tax in South Dakota if they gross more than $100,000 in sales of tangible personal property to residents of South Dakota in a given year OR conduct more than 200 such separate transactions.

And just like that, with Quill no longer restricting them, other states are free to expand their definition of nexus beyond physical presence as well.

In this article, we’ll unpack what this means to you as a business owner.

Is This Good News or Bad News?

Without knowing exactly what actions individual states will take in response, it’s too soon to tell. If the decision leads states to adopt more uniform sales tax rules, that would be good. But if it allows states to overreach and unnecessarily complicate online business, it could be bad.

Opponents of the decision to overrule Quill and uphold South Dakota’s law believe that allowing states to require sales-tax collection on online sales without the physical-presence restriction will overburden small businesses. They believe more extreme versions of sales-tax laws than South Dakota’s will be the result.

They also fear that the cost of doing business online will become prohibitive to all but the largest retailers.

Meanwhile, those in agreement with the decision to overrule Quill and uphold South Dakota’s law believe that large online retailers, who in some cases advertised “you don’t have to pay sales tax” as a benefit of shopping with them, were in essence enabling tax evasion on the part of shoppers, adding to the state budget deficits, and benefiting from an unfair advantage over retailers who do have a physical presence in a given state.

Another concern was the incentive by some large businesses to avoid a physical presence in certain states and the possible harm to the economies there. Some also feared that the states’ multitude of workarounds to the physical-presence rule would continue to grow while the set of rules online sellers are subjected to when it comes to sales tax would become impossible for small businesses to follow.

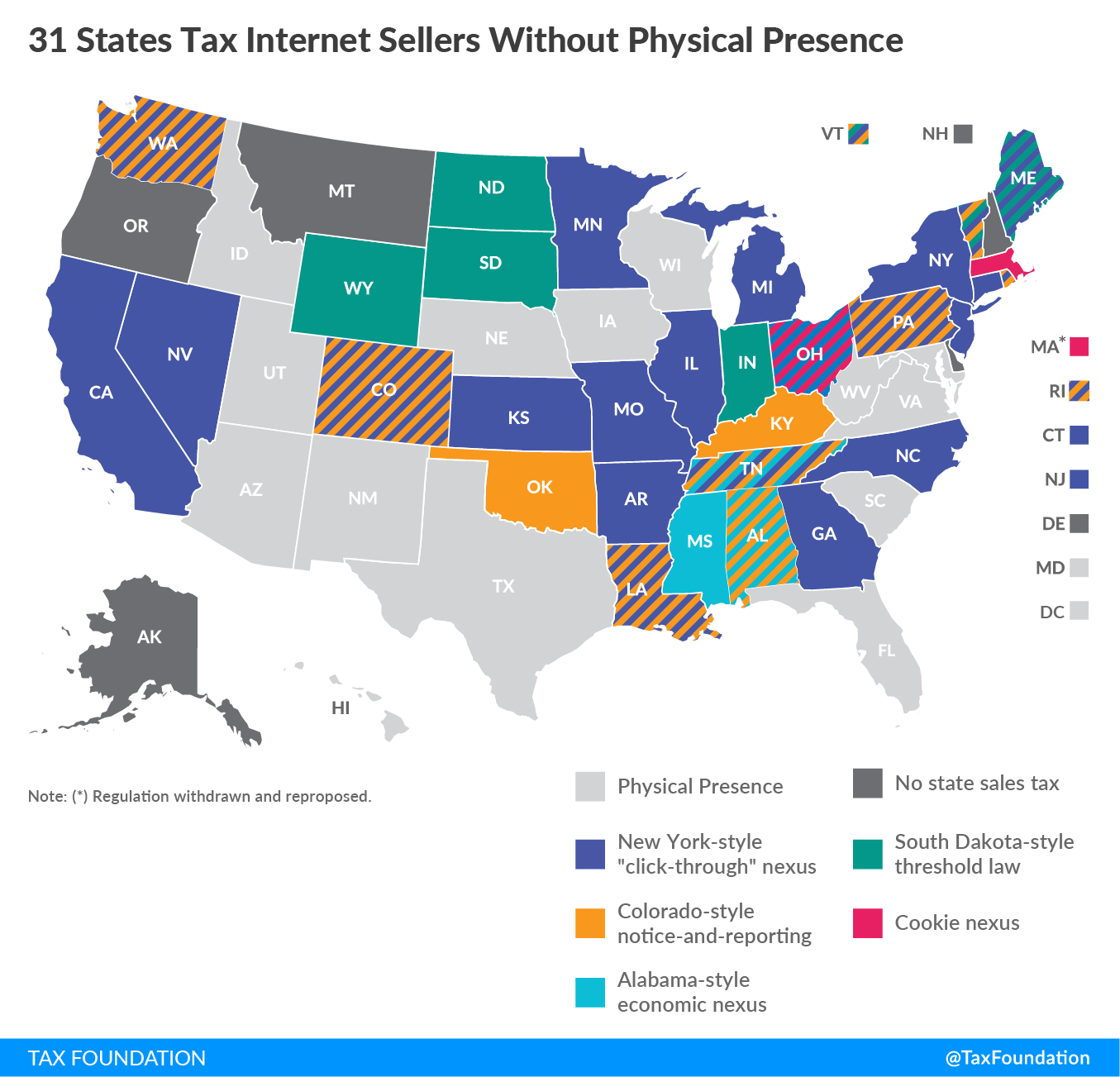

The fact is that 31 states already have laws in effect that tax internet sales by out-of-state sellers, and many of those are more complex and roundabout than the South Dakota law that was just upheld. Some of the workarounds to the physical-presence rule upheld by Quill that states have already put in place include:

- Expansion of nexus to include “click-through” and affiliate relationships.

- Expansion of nexus by invoking “economic nexus.”

- Threshold laws – like South Dakota’s.

- “Notice and reporting laws,” such as the one passed by Colorado last year.

- Expansion of nexus by creating “cookie nexus” as Massachusetts has tried to do.

Now that the court has decided to overrule Quill, effectively eliminating the physical-presence requirement in online sales-tax collection, there’s pressure on Congress to clearly define nexus in a way that’s relevant to today’s economy but still protects small business. Leaving the door open to even more complicated and varied rules for online businesses to sort through seems out of the question.

Curious how we got here? Keep reading...

Events Leading Up to This Decision

In 1992, the Supreme Court ruled in Quill v. North Dakota that states could not legally require out-of-state sellers who had no physical presence there (such as the mail order catalogs of the day) to register and collect sales tax for them. Instead, it would remain up to consumers to pay use tax to their resident states where sales tax was not charged.

As online sales volume ramped up, and brick-and-mortar retail sales declined, states searched for ways to collect the tax they were legally due from sales made by large online retailers. Congress had the power to pass federal legislation that would regulate the obligation of online retailers to states, but they did not.

South Dakota passed an economic nexus law that skirted the physical presence requirement, and Wayfair and other large retailers refused to comply, challenging the law as unconstitutional. South Dakota sued those retailers (Wayfair, Newegg, and Overstock.com), appealing the lower court ruling against them to the Supreme Court. As part of their case, South Dakota agreed in advance not to collect the tax retroactively from retail businesses and signed on to the Streamlined Sales and Use Tax Agreement, which seeks to minimize the cost and admin burden on retailers.

Lots of legal briefs were filed with the Supreme Court on both sides in reaction to the case. Meanwhile, Congress failed to act on several pieces of proposed legislation meant to clarify and delineate the states’ taxing powers over internet sales while they waited on the SCOTUS decision.

Last week, the Court decided in favor of South Dakota and said that the law they passed does not burden interstate commerce and can stand as is (with its restrictions on the burden it can place on businesses already in place). They ruled that the decision in Quill to define nexus based on physical presence was no longer relevant in today’s economy.

Why Now?

The sheer volume of transactions made across state lines daily and the billions of dollars at stake finally created a tipping point.

SCOTUS has explained its reasoning for overruling Quill in this way:

- The physical presence rule no longer reflects economic reality as a physical presence isn’t necessary to transact massive business within a state.

- Quill creates incentives for businesses to avoid setting up distribution channels or employment centers in certain states just to avoid the tax implications. Keeping Quill in place, “deprives states of vast revenues from major businesses.”

- South Dakota’s law affords small businesses a reasonable degree of protection.

The Court made the point that issues that could harm small businesses, such as new laws that apply retroactively (which South Dakota’s will not), a lack of uniformity from one locale to the next, and the possibility of other states not putting thresholds in place, were not before the Supreme Court to decide at this time. That reality may spur Congress to finally act.

Implications for Online Retail as a Whole

While large online retailers such as Amazon were given an advantage due to Quill when they first started out, many now collect sales tax on the majority of sales. Some, like Wayfair, have said publicly that the decision won’t have a drastic impact on their current business. Still, stocks in companies such as Amazon and Overstock.com took a hit as investors reacted to the decision.

On the whole, the same technology that allowed for explosive growth in ecommerce and spurred the states to act will help reduce the impact of the SCOTUS decision across the industry. Software like LumaTax allows even smaller companies now to easily file and pay sales tax to the proper state, while online shopping carts and merchant services like Square can be set up to automatically collect the tax.

It’s a safe bet that states will act now to collect tax on online sales in one way or another. But that reality seems unlikely to hurt or slow the growth of those sales to a noticeable degree. The momentum behind that growth at this point is simply too great.

Implications for Small Business

Much of the reaction in the small business community so far is based more on speculation around what states might do than on any immediate effects of this decision. If you make sales in South Dakota totaling more than 200 transactions or over $100,000 in a year’s time, you’ll need to register to collect sales tax with the state’s Department of Revenue now and know the correct rate.

While the cost of selling online across state lines will definitely go up for some, we still don’t know what thresholds other states will put in place before sales-tax requirements kick in. So it’s not a given yet that every small business will be affected. If you don’t sell online or ship products out of state, it’s likely that nothing will change for you.

Remember that it’s yet to be seen what action, if any, Congress will take to limit the reach of the states. There’s no reason for small ecomm businesses to panic yet, but it is a great time to consult with an accountant who will be tracking all the changes to the laws.

Meanwhile much of the technology needed to automate sales-tax collection, reporting, and payment is already available and more affordable now than it’s ever been.

What Do You Need to Do Now?

Stay tuned: States are in the process of reacting to the SCOTUS ruling. Keep in mind those 31 states that already have rules that may affect you, and watch for new tax rules in states where you haven’t had to collect so far. As we mentioned before, be on the lookout for any action that Congress takes that could influence your business in the future.

A few steps to consider as the states react to the decision:

- Check in with your accountant now or consider hiring one in the near future to ensure you’re in the loop on any changes to the law going forward.

- If you don’t already use it, start evaluating tax software options that will keep your business in compliance automatically.

- Be ready to update your shopping carts and point-of-sale systems to reflect new tax rates. Square users can see our guide to setting up sales tax here.

- Use our state-by-state tax guides to check the rules already in place in those states where you currently make sales and follow the links there to check for updates.

Frequently asked questions

What was the outcome of the Wayfair case?

The Supreme Court overturned the 1992 Quill ruling, eliminating the physical presence rule. Now, states can require online sellers to collect and remit sales tax if they meet certain economic thresholds—such as $100,000 in sales or 200 transactions in a state.

How does this affect online businesses?

Online sellers that exceed a state’s economic nexus threshold must register, collect, and remit sales tax, even without a physical location. Small businesses with limited out-of-state sales may remain unaffected, but compliance complexity will increase overall.

What should businesses do to stay compliant?

Businesses should review their sales activity by state, monitor evolving state thresholds, and consider using automated tax software like LumaTax to simplify registration, filing, and ongoing compliance across multiple jurisdictions.

{kind=link}