Key takeaways

- Public Law 86-272 limits state income tax on out-of-state sellers: It protects businesses whose only in-state activity is soliciting sales of tangible goods, but recent reinterpretations have narrowed that protection.

- States are updating their guidance for the digital age: California’s adoption of the Multistate Tax Commission’s 2021 interpretation means many online activities—like cookies, chat support, and post-sale services—may now create tax obligations.

- Businesses must reassess compliance risks: With more states expected to follow California’s lead, companies engaged in e-commerce should review their activities and consider disclosure programs to mitigate exposure.

Public Law 86-272 is a federal law that prohibits states and localities from imposing income taxes on out-of-state businesses if their only activity within a state is soliciting sales of tangible personal property. This law prevents states from asserting their right to impose a tax based on net income, such as corporate income tax or franchise tax.

Initially enacted in 1959, many states recently examined and re-examined P.L. 86-272 in an effort to pinpoint its most accurate application in relation to modern e-commerce – a business category that didn’t exist when the law was written.

In August 2021, the Multistate Tax Commission (MTC) re-interpreted Federal Public Law 86-272 and, in doing so, effectively removed several significant out-of-state retailer protections from state income tax. These protections had been in place since the law’s inception over sixty years, though they became significantly more relevant in the past couple of decades.

Unfortunately, the MTC made a sweeping statement that, if widely adopted, has the potential to harm small and mid-size businesses. Online Merchant’s Guild Executive Director, Paul Rafelson, expressed his concern in a recent Bloomberg article. He said, “It’s like (the MTC) doesn’t understand the difference between Google and a kitchen table sales enterprise. If every other state starts doing this, we’re toast.”

In response to backlash over their statement, MTC council member and the lead author of the commission’s interpretation, Brain Hamer, said, “This is not a change but an effort to apply a 60-year-old statute to modern facts. It is incumbent upon the states themselves to interpret that statute until the courts say otherwise.” With that, he essentially passed responsibility to states. Let’s look at two drastically different examples of how they’re responding.

State Interpretations of P.L. 86-272

Some states issued detailed guidelines around how P.L. 86-272 impacts their tax laws before the conversation around the federal law became national news in 2022. For example, New Mexico published a highly detailed tax information briefing, revised in July 2020, that provides business owners with information on their interpretation of P.L. 86-272.

Here’s some of the language found in that briefing.

New Mexico requires corporations to meet all of the following criteria to be immune to taxation under P.L. 86-272:

- The corporation does not maintain a business location or office in New Mexico.

- The corporation is not incorporated in New Mexico.

- All sales occur in interstate commerce.

- The corporation sells only tangible personal property in the state. Immunity does not extend to a corporation that leases, rents, or licenses tangible personal property or conducts transactions involving such intangibles as franchises, patents, copyrights, trademarks, and the like.

- All sales solicited in New Mexico are contingent on approval (acceptance) outside the state. To retain immunity from corporate income tax under P.L. 86-272, a corporation must limit its activities in New Mexico to soliciting sales of tangible personal property.

In addition to detailing how corporations can be immune to tax, New Mexico also specific various types of business activities that are considered “protected” from P.L. 86-272.

When performing these activities, in conjunction with soliciting sales of tangible personal property, New Mexico corporations are immune under P.L. 86-272:

- Soliciting orders by any medium of advertising.

- Soliciting orders through an in-state resident employee or corporation representative.

- Carrying samples and promotional materials only for display or distribution.

- Furnishing and setting up display racks and advising customers on the display.

- Providing automobiles to sales personnel for their use in conducting protected activities.

- Passing orders, inquiries, and complaints to the home office.

- Missionary sales activities; that is, soliciting indirect customers for the company's goods.

- Coordinating shipment or delivery and providing information about shipment or delivery.

- Checking customers' inventories without charge for reorder but not for other purposes.

- Maintaining a sample or display room for up to two weeks (14 days) at any one location.

- Recruiting, training, or evaluating sales personnel.

- Mediating direct customer complaints with a sole purpose of ingratiating sales personnel with the customer and facilitating requests for orders.

- Owning, leasing, using, or maintaining personal property for use in the employee's or representative's in-home office.

The state also provides specific rules for independent contractors, which allow them to retain immunity in the state under certain conditions.

Lastly, in addition to specifying which business activities are protected from P.L. 86-272, New Mexico clearly defines what types of activities are considered unprotected.

Here are a few specific examples:

- Making repairs or providing maintenance or service to the property sold or to be sold.

- Collecting current or delinquent accounts directly or by third parties.

- Investigating creditworthiness.

- Installing or supervising installation during or after shipment or delivery.

- Conducting training courses, seminars, or lectures for personnel other than personnel involved in solicitation only.

- Providing any kind of technical assistance or service, including but not limited to engineering assistance or design service, when one of the purposes is other than to facilitate the solicitation of orders.

- Approving or accepting orders.

This list is far from exhaustive, but it gives you an idea of the level of detail some states are providing as they evaluate their stance on how this federal law influences businesses’ tax obligations in their state. Clearly, New Mexico is being very thoughtful about the potential impact businesses may face as a result of any changes that are made in relation to this law.

Now, let’s look at a state that went an entirely different direction with its interpretation, this one released on the coattails of MTC’s statement in February 2022.

California Follows in the MTC’s Footsteps

Earlier this year, the California State Franchise Tax Board (FTB) issued a memorandum stating that they plan to essentially echo the MTC’s re-interpretation of the law within the state. They communicated this by issuing a Technical Advice Memorandum, which details twelve different business activity “Fact Patterns” and provides reasoning on why each one is considered ‘protected’ or ‘unprotected’ from taxes.

The memorandum reads:

The FTB's positions on protected and unprotected internet activities largely follow those expressed in the recently revised Statement of Information concerning practices of the MTC and supporting states under P.L. 86-272 (Statement) issued by the Multistate Tax Commission (MTC), without specifically adopting or referencing the Statement.

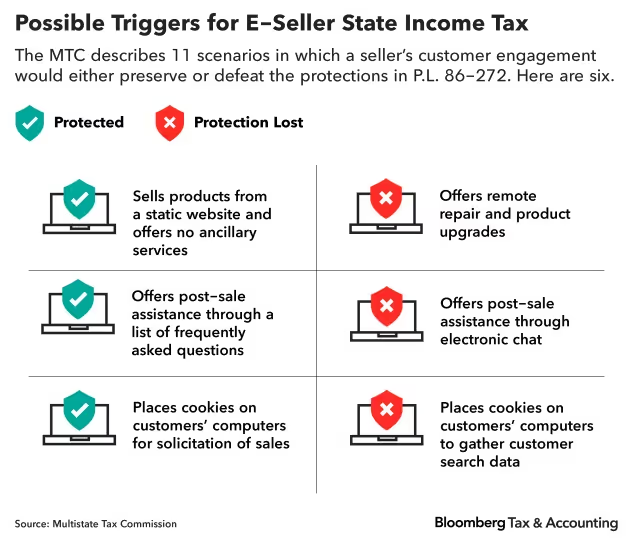

Under TAM 2022-01, the FTB deems the following to be protected business activities:

- Providing post-sale assistance to California customers by posting a static list of frequently asked questions on the business's website.

- Placing on California customers' computers or other electronic devices "cookies" that gather customer information for uses "entirely ancillary" to soliciting orders for tangible personal property.

- Offering only tangible personal property for sale on the business's website, with the website allowing customers to search for items, read product descriptions, purchase items, and select delivery options.

Under TAM 2022-01, FTB deems the following to be unprotected business activities:

- Having an employee who telecommutes from California on a regular basis performing non-sales solicitation activities (e.g., business management and accounting tasks).

- Regularly providing post-sale assistance to California customers through an electronic chat or email that customers initiate by clicking on an icon on the business's website.

- Soliciting and receiving online applications for its branded credit card through the business's website

- Placing on the business's website an invitation for California viewers to apply for non-sales positions within the business.

- Placing on California customers' computers or other electronic devices "cookies" that gather customer search information for use in adjusting production schedules and inventory amounts, developing new products, or identifying new items to offer for sale

- Remotely fixing or upgrading California customers' previously purchased products by transmitting code or other electronic instructions to those products over the internet.

- Offering and selling extended warranty plans through the business's website to California customers who purchase the business's products.

- Contracting with a marketplace facilitator to facilitate the sale of the business's products on the marketplace facilitator's online marketplace, where the marketplace facilitator maintains inventory, including that of the business, at fulfillment centers in a state in which the business's customers are located.

- Contracting with California customers to stream videos and music to electronic devices for a charge.

The FTB closes with a summary statement, which reads, "an Internet seller is shielded from taxation in the customer's state if the only business activity it engages in within that state is the solicitation of orders for sales of tangible personal property, which orders are sent outside that state for approval or rejection, and if approved, are shipped from a point outside of that state."

Implications of California’s New Stance on P.L. 86-272

The state's new interpretation removes tax immunity protections for sellers that perform certain activities on their website, including things like providing product support, installing cookies to gather customer search data, and providing post-sale chat support on their website.

With these changes in place, tens of thousands of businesses previously exempt from California state taxes are now responsible for collecting and remitting money to the state. That means many businesses face a loss of tax protections they relied on to protect their profit margins.

California’s memorandum goes on to state, “Out-of-state businesses conducting activities that were not previously listed as unprotected activities in the FTB's Publication 1050 should consider evaluating their California activities and determine whether those activities continue to fall within that protection.”

The bulletin also specifies that companies need to re-evaluate if their company website is engaging in business activities that are considered to be “unprotected” under this new interpretation. It goes on to say there is no effective date listed, making it unclear whether or not this guidance applies beginning in 2022 or whether it will be applied retroactively if a business neglected to pay taxes in prior years. A statement released by the state encouraged businesses to consider utilizing California’s voluntary disclosure program if they have concerns surrounding the impact of these new guidelines.

What Happens if the MTC’s New Interpretation is Widely Adopted by States

Additional states are anticipated to follow in California’s footsteps by adopting a mostly verbatim approach to their own re-interpretations of P.L. 86-727. Doing so presents a significant upside (read: profits) for state tax authorities.

States taking a stance on their individual interpretations of 86-272 will result in more tax complexity. This means businesses already facing significant tax confusion will struggle even more to ensure they’re accurately collecting and remitting taxes to various states. As audits start to take place, we can also anticipate that businesses will begin filing lawsuits against states to fight changes they feel present an unfair disadvantage to their company.

How to Help Your Clients Navigate P.L. 86-272 Tax Complexity

Compliance is costly, but non-compliance is even more expensive – particularly for businesses that are intentionally or unintentionally ignorant of their tax responsibilities. As a trusted accounting resource for small and mid-size business owners, it’s important that you stay on top of new state guidance or legislation that comes out in response to the MTC’s statement on P.L. 86-272. If you’re not already working with LumaTax to be able to support your clients in the most effective way possible, it’s the perfect time to partner with us. We’ll help you stay on top of changes, keep your clients compliant, and boost your advisory service offerings and profits.

Frequently asked questions

What is Public Law 86-272?

Public Law 86-272 is a federal law that protects out-of-state businesses from state income tax if their only in-state activity is soliciting sales of tangible personal property. It prevents states from taxing income based solely on minimal sales solicitation activity.

Why is P.L. 86-272 being reinterpreted?

The law was written in 1959, long before e-commerce existed. The Multistate Tax Commission (MTC) reinterpreted it in 2021 to reflect modern business activities like online sales and digital interactions, which were not originally addressed.

How are states responding to the new interpretation?

Responses vary. Some states, like New Mexico, have issued detailed guidance clarifying protected activities. Others, such as California, have adopted the MTC’s broader interpretation, removing many online seller protections and expanding tax obligations for remote businesses.

What should businesses do next?

Companies selling across state lines should review their online activities—such as chat support, cookies, and post-sale services—to determine if they now create tax nexus. Consulting with a tax expert or using compliance tools like LumaTax can help ensure ongoing compliance.