.png)

Key takeaways

- Wayfair expanded tax obligations: Businesses must register and collect sales tax in every state where they have nexus.

- Proactive compliance prevents penalties: Regularly track sales thresholds and register on time to avoid costly fines.

- Standardized processes save time: Use clear workflows and multi-state registration tools to simplify SUT compliance.

Thanks to the South Dakota v. Wayfair supreme court ruling, businesses that previously had no requirement to register and collect sales tax must now comply with multi-jurisdictional laws and stay up-to-date on tax rate and law changes. Applying for a sales tax permit in each nexus state is a crucial compliance step. There are a lot of intricacies involved in this process - especially for remote sellers, e-commerce companies, non-US-based organizations with inbound US sales, and companies with limited nexus obligations.

State Registration 101

When a business establishes nexus in a new state, the owners must obtain a sales tax permit, also called a seller’s permit, before collecting and remitting tax. Creating this agreement between the business and the state tax agency gives the business permission to collect and remit sales tax on items they sell.

It takes substantial time to research exactly what each state requires to correctly set up shop in their jurisdiction. Most businesses don’t have the resources to handle the task from start to finish, which is why CPAs often find themselves involved in this process.

The complexity surrounding this process often leads to easily avoidable mistakes. However, you can sidestep these state registration compliance faux pas if you know what to look for. Here are eight of the most common issues we see and steps you can take to help clients avoid them.

Issue #1: Not Consistently Tracking Sales Against Nexus Thresholds

Everything begins with nexus. Economic nexus is the primary factor for most businesses, but thresholds are far from one size fits all. They’re different in every state, both in number and in the types of sales that count (or don’t count) toward economic threshold receipt totals.

To stay compliant, businesses need to know how their sales are tracking to economic nexus thresholds - both monetary and transaction count. It’s also essential to meet state registration deadlines once the nexus is triggered.

Business owners should work with their CPA to develop a clearly defined process for regularly monitoring thresholds - be it quarterly or monthly. It’s also important to document who’s responsible for each stage of the process - the business owner or the CPA.

Issue #2: Missing Nexus Obligations Due to Incomplete Data

We can’t tell you how often we see nexus studies run with incomplete data. If any transactions are missing, the nexus study renders false results.

Businesses often turn to their general ledger or raw data files to pull transaction data for a nexus study. However, a general ledger may lack critical data needed to assess and identify nexus. For example, revenue reports are often insufficient, integrations commonly omit data in the import process, and sales tax liability reports can be deeply flawed. Raw data files also present challenges because they often show invoice-level data rather than line-level data, have inconsistently formatted dates, contain billing and shipping address inaccuracies, including missing or incomplete zip codes.

As the expert resource, CPAs should help clients identify the data they need to pull and help them set up an accurate nexus tracking report.

For a complete report, you need to extract the following details (at minimum) for every transaction:

- Transaction date

- Invoice number

- Ship-to or transaction location (full address)

- Total invoice amount

- Total sales tax collected

CPAs must work with their clients to identify all source systems to find these details. This includes invoicing systems. You’ll also need access to online shop and marketplace data from platforms like Shopify or Amazon, as well as 3PL (third party warehouse, inventory management, and fulfillment) data.

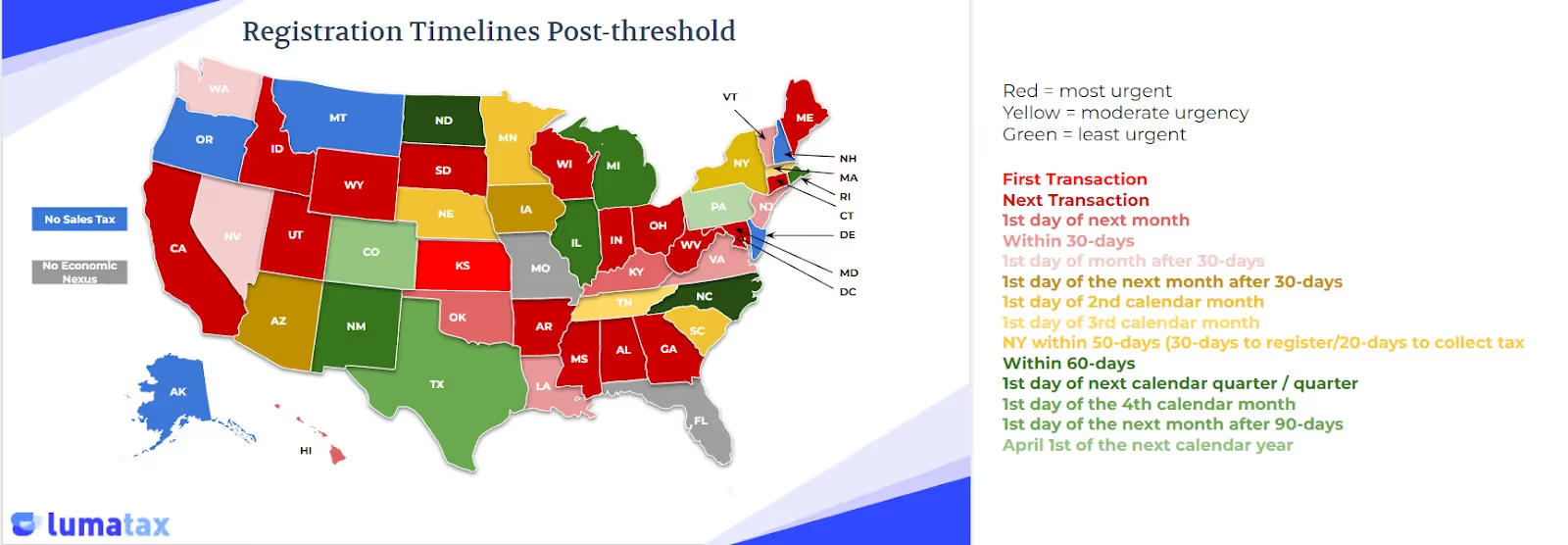

Issue #3: Keeping Track of Registration Deadlines

Here’s how states are currently managing nexus registration deadlines:

Not only is it messy, but rules change frequently.

Your team needs to have organized, up-to-date registration details available to provide the best SUT advisory services. This step will help you ensure that your clients register with appropriate states and collect and remit tax on time, keeping them safe from costly penalties.

Issue #4: Taking an “Ask for Forgiveness Later” Approach

It’s all too common for businesses to realize they crossed a threshold but decide to wait and see what happens. Many believe that it will take a long time for states to realize they owe tax, but that’s not a smart way to handle things. In fact, there are many reasons you should encourage clients not to take this approach.

Specifically:

- 1. States have become increasingly aggressive about finding out-of-state sellers who are required to register in the state. How? They have a lot of tools at their disposal, including data analytics, the use of purchased data, web searches, and more.

- 2. In the wake of the Wayfair decision, some states - including but not limited to California, Washington, and New York - subpoenaed Amazon to provide their state Department of Revenue with lists of third-party sellers that have in-state inventory.

- 3. If a business that's required to register but hasn't gets audited, penalties are far steeper than they would be if the business had registered when they established nexus.

Your team needs to be able to counsel clients on the ramifications they may face if they opt to take this unfavorable approach. Assess risk factors and advise clients with the highest likelihood of incurring penalties first.

Issue #5: Not Knowing Which Type of Sales Permit to Apply For

Registering for a sales permit should be pretty straightforward, but it can be confusing. States offer different types of permits or licenses to sellers based on how they sell.

For example, permits often differ for in-state businesses collecting tax based on physical presence nexus versus out-of-state companies collecting tax on remote sales because many states use different tax forms for each type of tax. Ensuring the correct permit is selected during setup will make things far easier when it comes time to remit tax to the state.

CPAs should know about the different types of seller permits states require and any specific state tax programs your clients can take advantage of. Staying up to date on all of these critical factors will allow you to provide the best possible SUT advisory to your clients.

Issue #6: Being Reactive, Not Proactive with SUT Compliance

When a client comes to you with an issue that could have been avoided, your team has to work to untangle a nexus-fueled mess - a less than ideal yet very common scenario.

In this situation, your client has to 1) ignore the interim period of non-compliance or 2) file a late return, thereby incurring penalties and interest. As their trusted advisor, you must inform your client that the state registration document is signed under penalty of perjury. A representative of the client has to declare a business start date in the taxing jurisdiction. If the start date is before the timely registration date, it’s likely to trigger an inquiry for the missed filing periods. However, if they write the current date as the start date, there’ll be a problem with the attestation on the registration.

To avoid this scenario altogether, it’s best to have a proactive SUT advisory program in place. This allows you to evaluate your client’s sales activities before they’ve exceeded any economic nexus thresholds and gives you a concrete understanding of where your client has post-Wayfair economic nexus requirements. When proactive management is in place, a timely registration for a sales and use tax license is an easy step.

Issue #7: Data Gathering for Registration is a Massive Undertaking

State tax registrations ask for an outrageous amount of information. Like what? Businesses need to have the following handy to fill out registration applications:

- Corporate information

- Business activity (NAICS Codes, TPP)

- Ownership information (including sensitive personal information)

- Accounting information (applicant must know where to find relevant books and records)

- License information, which includes being able to identify the right license type

You also need all your business information, including common biographical characteristics, tax liability start dates, and answers to physical presence questions - (number of employees, etc.). If you’re working with a non-US-based business client? The list gets even more nuanced.

It’s a process to have all this information ready in a secure place, but it’s worth the amount of time it saves to prepare your clients for what they’ll need ahead of time.

Issue #8: Unresolved Physical Nexus Issues Impact Date of First Business

During the registration process, your client taxpayer will be asked for the “date of first business,” “date of first transaction,” or “date nexus first established.” They will also have to assert under penalty of perjury or attest under state law that the application is true and correct.

The problem is many business owners put conflicting information in their application by listing dates or facts that contradict the “date of first transaction” they submit. For example, a business can establish physical nexus based on the number of employees they have in a state, holding inventory in a state, and so on.

If these things are recorded improperly, it can change or alter the date nexus was established, therefore changing the period in which they should have been collecting and remitting tax within the state. Watch for all these possible triggers to help clients stay on top of nexus registrations.

Best Practices to Streamline SUT Advisory

If you’re just now talking to your clients about Wayfair compliance, you’re behind the curve. Wayfair has been the law for over two years, and all but two states have implemented legislation to adopt it. However, it’s not too late to adopt and implement a proactive SUT advisory approach. We recommend taking the following steps as soon as possible.

#1: Create an Action Plan

The bottom line is compliance with the law is expensive for businesses, but non-compliance is even more expensive. To set your clients up for success, it’s a great idea to create a formal, documented plan that you can provide to your clients and circulate it within your firm- present best practices at partner sessions, educational meetings, and so on.

An ideal plan will:

1. Focus on economic nexus.

2. Overlay physical nexus when applicable to identify and remediate unresolved physical nexus issues caused by distributed workforces or FBA and 3PL inventory.

3. Include a “registration trigger” workflow and define what those triggers are (sales volume, transaction volume, new employees, distributed workforces, independent contractors, inventory locations.

4. Be circulated internally with details on how to identify high-risk clients (those doing $3M+ in ARR; merchandisers, those in the digital goods space, and SaaS companies, clients that have one state registration.

Developing an action plan will allow you to adopt a proactive approach to SUT advisory.

#2: Survey Clients to Identify Those with the Highest Risk

Now it’s your turn to run inventory - on your clients! Take a look at the accounts you’re supporting and look for red flags. If you find any businesses that are showing signs of potential noncompliance, it may be time to do a nexus study to identify their registration needs.

#3: Take Advantage of Multi-State Registrations

There's a component of streamlined sales tax that allows businesses to register with multiple states through one application. This can be a big timesaver and should always be used when it's in the client's best interest. Make sure your team is well-versed in this option.

Frequently asked questions

What is a sales tax permit, and why do businesses need one?

A sales tax permit (or seller’s permit) authorizes a business to collect and remit sales tax in a state where it has nexus. It’s a legal requirement before collecting any tax from customers.

When should a business register for sales tax?

Businesses must register once they cross a state’s nexus threshold—either through economic activity (sales or transactions) or physical presence (employees, inventory, etc.). Each state has different thresholds and registration deadlines.

What are the biggest mistakes companies make when registering?

Common issues include missing or inaccurate data, applying for the wrong permit type, and failing to register on time after triggering nexus. These errors can lead to penalties, audits, and compliance backlogs.

How can businesses simplify multi-state tax registration?

Using the Streamlined Sales Tax Registration System allows companies to register with multiple states through one application, saving time and ensuring consistent compliance.

How can CPAs help clients stay compliant post-Wayfair?

CPAs should proactively track clients’ sales data, identify nexus risks early, and create structured workflows for registration and ongoing SUT (sales and use tax) compliance.